A Comprehensive Analysis of Arista Networks

A Comprehensive Analysis of Arista Networks

Financial Stability and strong growth prospects?

Introduction

This article offers an insightful look into Arista Networks, a key player in the networking industry. It reveals that Arista is thriving financially, with impressive sales growth and solid returns on investments. The company's strategic handling of debt and assets highlights its robust financial foundation. Additionally, the growing online interest in Arista and positive feedback from both employees and customers paint a picture of a well-regarded company. A valuation analysis, however, presents a nuanced perspective, indicating that the stock's value might be subject to different interpretations based on growth calculations.

Business Overview

Arista Networks is a company that makes and sells networking solutions for big data centers, campuses, and routing areas. It started in 2004 and is located in Santa Clara, California. The company creates network switches used for data centers, cloud computing, and high-frequency trading.

Arista's products include network operating systems, Ethernet switches, and routing platforms. They offer solutions for cloud routing, campus networks, infrastructure networking, electronic trading, hybrid cloud, and big data. They focus on making networks that are reliable, fast, automatic, and secure.

Most of Arista's sales come from products (about 85%), with the rest from services. They sell mostly in the Americas, but also in Europe, the Middle East, Africa, and Asia-Pacific. Arista Networks has over 3,600 employees. They work with different types of customers, like internet companies, service providers, financial groups, government agencies, and media and entertainment companies.

Quantitave Analysis

Performance

Average Revenue Growth Rate: Over the past 10 years, Arista Networks' average annual revenue growth rate has been approximately 38.72%. This indicates a strong and consistent increase in the company's sales year over year.

Source: stockanalysis.com Average Return on Equity (ROE): The average ROE for the past years is around 25.74%. This high average suggests that Arista Networks has been very effective in generating profits from its shareholders' equity.

Average Return on Invested Capital (ROIC): The average ROIC stands at about 22.59%. This figure shows that the company has been successful in using its capital investments to generate returns, underlining its efficient capital management.

Average Return on Assets (ROA): With an average ROA of approximately 15.69%, Arista Networks demonstrates a strong capability to generate earnings from its asset base.

These averages reflect Arista Networks' robust financial health and efficiency, showcasing its ability to grow revenue, effectively use shareholders' equity, manage its investments, and utilize its assets to generate profits

Financial Solidity

Arista Networks showcases exceptional financial strength, as evidenced by its low Debt-to-Equity ratios and high Current Ratios over several years. The low Debt-to-Equity ratios, that have never been higher than 0.1, illustrate a strategic avoidance of excessive debt and a preference for equity financing. This approach signifies a cautious and risk-averse financial strategy. Complementing this, the company's Current Ratios, consistently above 4, demonstrate a robust liquidity position, ensuring that Arista has the assets to greatly meet its short-term liabilities. Together, these metrics underscore Arista's solid financial foundation, prudent capital management, and its strategic commitment to maintaining financial stability and operational flexibility.

Valuation

In the DCF analysis of Arista Networks, I excluded the considerable growth of 2013 for the average growth calculation, focusing on 2014-2022 because i believe such growth is highly uncertain considering its current size. This resulted in an average growth rate of 48.43%, leading to an intrinsic value of $472.93, using a perpetual growth rate of 2.5% and a discount rate of 8.5%. However, this value might be skewed by the exceptional growth between 2016 and 2017. In contrast, applying the median growth rate of 32.15% with the same perpetual growth rate and discount factor, the intrinsic value is calculated at $181.02 which is lower than current price of $217. However Arista's strong Return on Capital should also be considered as a vital growth indicator, potentially justifying a higher valuation.

Qualitative Analysis

Interest

The Google Trends graph shows that more people have been looking up Arista Networks on the internet over the last year. This means the company is getting more attention and could be drawing in more customers.

Reviews

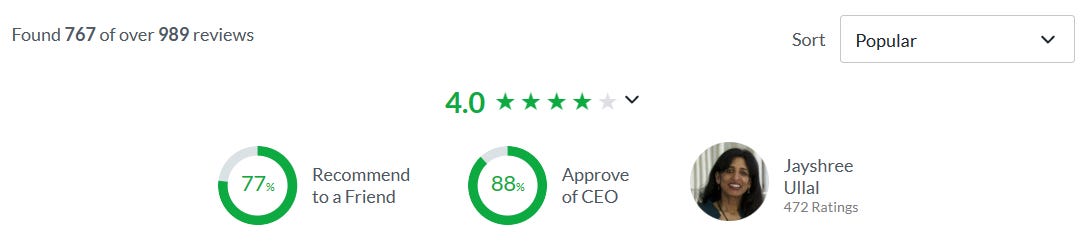

Employees

The reviews from Glassdoor.com show that it enjoys strong support from its employees. A majority of the staff appreciate the smart colleagues and good work-life balance, and they speak highly of the company's culture and management. The CEO has a high approval rating, and a significant number of employees would recommend working here to a friend.

Customers

Arista Networks has received outstanding feedback from its customers, as seen in the high ratings across several key areas. The company's overall customer satisfaction score is an impressive 4.7 out of 5 stars, with the vast majority of ratings being perfect scores. Customers consistently rate their experience with Arista's services and products very highly, particularly praising the company's integration and deployment process. The strong customer endorsement is further reinforced by the fact that 94% of customers say they would recommend Arista Networks, underscoring the company's success in delivering quality products and services that meet the needs of its users.

Conclusion

In conclusion, Arista Networks stands out as a financially secure company with promising growth prospects even though it may potentially be somewhat overlypriced. This aligns well with Warren Buffett's quote: “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price”. Arista's strong performance and positive market perception suggest it is a high-quality business that merits consideration for its growth value.